Unpacking Covid-19’s Varied Impacts within an Agrifood Industry: A Case Study of Japan’s Wagyu Industry

Volume 26, Issue 1 (Article 2 in 2026). First published in ejcjs on 23 April 2026.

Abstract

The Covid-19 pandemic disrupted food systems in complex ways that agrifood scholars are still unpacking. This article reports on Covid-19’s impacts on heirloom Japanese beef industry, also known as the wagyu industry. By focusing on variation within an industry that endured significant disruption, our research highlights the complex role of industries and actors within the Covid-19 food crisis. This article reports on a survey of Japanese wagyu brands through which we received 101 responses (45.1% response rate). The survey responses showed that when comparing the November 2022 industry to pre-pandemic conditions, sales, production, and value decreased with the sharpest decline occurring in restaurant sales. Despite these decreases, total production maintained and internet sales increased. When controlling for brand size, medium-size brands tended to face the sharpest contraction. In contrast to these general trends, however, numerous exceptions emerge that highlight the importance of the varying conditions facing and responses taken by individual brands. In conclusion, we argue for examining how situated actors and organisations respond to disruptions like Covid-19. For wagyu, we emphasise greater recognition of how distinct brands with differing circumstances and trajectories constitute the wagyu industry.

Keywords: wagyu, Japan, artisan brand, Covid-19, food system.

Introduction

In the face of the disruption from Covid-19, a broad range of businesses appealed to the Japanese government for assistance, including the restaurant, hotel, and air travel industries. In terms of food consumption behaviour, consumption patterns in Japan shifted away from eating out and towards eating at home (Matsumoto and Otsuki, 2024). Although restaurants endured hardships, neighbourhood restaurants maintained an important role in local communities of facilitating conviviality and culinary practices (Farrer, 2022). As restaurants struggled, local food systems proved especially resilient at maintaining food access and security (Lichten and Kondo, 2020; Kamiyama et al., 2023). The Japanese government sought to provide support for industries suffering economic hardships during the pandemic. As a part of these efforts, the government set aside funds for artisan food such as wagyu (Japanese beef) and melons. Such artisan foods are typically viewed as luxuries consumed on festive occasions, and some criticised the government for diverting funds to support artisan producers (Kajimoto, 2020). Unlike local food and industrial food, artisan producers had less flexibility to shift away from in-person dining and towards other retail mechanisms such as in-store shopping or home delivery (Schrager and Kondo, 2024). Covid-19 struck artisan food hard but inconsistently. Some brands and actors were better positioned than others to adapt to the disruption accompanying Covid-19.

Most research on the food crisis accompanying Covid-19 focused on rising food insecurity (e.g. Altieri and Nicholls, 2020; Clapp and Moseley, 2020). These deprivations were severe and warrant close analysis. However, disruption to food systems from Covid-19 extended far beyond vulnerable populations suffering from heightened food insecurity. Rather than focusing on food insecurity, Schrager and Kondo (2024) develop a “critical agrarian approach to food crises” that builds on the surge of critical agrarian scholarship described by Edelman and Wolford (2017). In so doing, Schrager and Kondo situate food crises as introducing a spatiotemporal widening of possibilities for reconfiguring food systems. Such a reconfiguration originates from a specific crisis that intersects with the general food crisis of the corporate food regime. Specific crises like Covid-19 introduce an opportunity for change, but the direction and character of such change is complex and often defies generalisations across regions or industries. This complexity poses a unique analytical challenge for agrifood scholars, because Covid-19’s varied impacts may entice scholars to make overgeneralisations based on limited field research or media coverage. For example, some media coverage of Japan’s wagyu industry described it as falling into a state of crisis (Asahi Shimbun, 2020b; Asahi Shimbun, 2020a). While this was certainly true for some wagyu-affiliated operations and brands, we report in this article on a survey of wagyu brands regarding the impacts of Covid-19.

Referencing the 2021 Brand Beef Hand Book (sic) compendium of beef brands in Japan (Shokuniku Tsūshin-sha, 2021), we received survey responses from 101 wagyu brands regarding changes in production, sales, and characteristics comparing pre-pandemic conditions to November 2022 conditions. Our findings underscore the complexity of the pandemic’s impact on food systems. Surveyed brands reported more widespread declines in revenue than declines in production volume or sales volume. These declines were more widespread for medium-sized brands than large-sized or small-sized brands. In addition, about 10% of brands reported increases. Our survey also indicated widespread declines in sales to restaurants and increases in online sales. In addition, certified producers declined but certified retailers increased. These changes indicate a modest decline in medium-sized brands and a shift towards larger brands and operations. These shifts, however, cannot be reduced to a mere deepening or reversal of the larger crisis of the corporate food regime. Instead, these shifts are best understood as introducing new dynamics that will shape the foundation of the wagyu industry going forward.

In 2022, the Japanese government reported that beef production generated 826 billion yen of revenue (~$5.5 billion USD, 9.2% of overall revenue) (MAFF, 2023b). We estimate revenue from wagyu beef production to be roughly 500 billion yen (~$3.5 billion USD, 5.6% of overall revenue; we explain this estimate in more detail in the subsection ‘Current conditions’). Drawing from the survey data, this paper responds to two research questions. First, what were the varied impacts of Covid-19 on wagyu brands? And second, how does this inform our understanding of how food crises reshape food systems? Following from these research questions, this paper seeks to deepen both our understanding of wagyu and Covid-19’s impacts on food systems.

We structure the article by beginning with an introduction to the wagyu industry: its emergence, Covid-19’s impacts, and its current conditions. Then we introduce our survey results. Next, we discuss the survey results. In conclusion, we contextualise disruption and recovery from Covid-19.

Wagyu

Emergence of wagyu

Previous articles have examined the qualities of wagyu beef and characteristics of the wagyu beef industry (Motoyama, Sasaki and Watanabe, 2016; Gotoh et al., 2018). Here, we delve into areas seldom covered in English-language literature and examine the historical development of wagyu beef and the current relationship between the wagyu standard and individual wagyu brands. Our summary of this history draws from Ishihara (2023).

A historical document from the late Kamakura period (1185-1333) titled ‘Illustration of ten domestic cows’ (国牛十図) contains illustrations and descriptions of cows from the following ten regions: Chikushi Cattle (Present day Fukuoka Prefecture), Mikuriya Cattle (present day Nagasaki Prefecture), Awaji Cattle, (present day Hyogo Prefecture), Tajima Cattle (present day Hyōgo Prefecture), Tamba Cattle (present day Kyoto Prefecture and Hyōgo Prefecture), Yamato Cattle (present day Nara Prefecture), Kawachi Cattle (present day Osaka Prefecture), Tōtōmi Cattle (present day Shizuoka Prefecture), Echizen Cattle (present day Fukui Prefecture), and Echigo Cattle (present day Niigata Prefecture) (Ishihara, 2023, pp. 15–17). At the time, cattle were primarily used for transportation and to assist with agricultural labour such as plowing the fields. While cattle have a long history in Japan stretching back well over a thousand years (Hudson and Muñoz Fernández, 2023), the history of intentionally breeding cattle for meat consumption is far shorter and first emerges during the Meiji era (1868–1912). From the 1870s through the 1900s, Japan imported Western breeds of cattle, but livestock scientists struggled successfully to introduce improved breeds by crossing Western cattle with Japanese heirloom cattle.

The Japanese government launched a campaign to improve Japanese breeds (改良和種) in 1912 that encouraged organisations across Japan to experiment with crossing and improving cattle. Breeders sought to introduce hybrids from Japanese and Western breeds that were useful in terms of both farmwork and meat quality. In 1944, the Japanese government officially certified three Japanese wagyu breeds: Japanese Black (黒毛和種), Japanese Brown (褐毛和種), and Japanese Polled (無角和). Post-World War II, administration of Japanese cattle breeds shifted to the Wagyu Registry Association, which in 1957 recognised a fourth wagyu breed, Japanese Shorthorn (日本短角種). The Wagyu Registry Association continues to be a key organisation for wagyu, establishing regulations and maintaining a vast archive of wagyu cattle with information on cattle ancestry and quality. As tractors spread across Japan in the 1950s and 1960s, cows were no longer necessary for farmwork. With these changing circumstances, breeders selected exclusively for meat quality (Ishihara, 2023, p. 29).

Especially before the use of genetic analysis, random mutations and nonhuman actors left an indelible imprint on the early formation of wagyu. For example, a seed bull born in 1939 named Tajiri-gō (田尻号) was said to have sired 1,463 calves (Asahi Shimbun, 2012; Ishihara, 2023, p. 27). According to a genetic analysis conducted by the Wagyu Registry Association in 2012, 99.9% of Japanese Black wagyu are descendants of Tajiri-gō (Asahi Shimbun, 2012). Since 98% of wagyu are the Japanese Black wagyu breed, Tajiri-gō left an indelible hoofprint on Japanese wagyu (Ishihara, 2023, p. 39).

Aside from living actors like Tajiri-gō and livestock breeders, the Japanese standard for ranking meat quality had a far-reaching impact on the trajectory of farming, producing, and retailing of Japanese beef. The Agriculture & Livestock Industries Corporation introduced a standard for ranking beef and pork quality in 1962 with the Ministry of Agriculture and Forestry’s encouragement. By the following year, inspectors graded meat at four wholesale markets, and this inspection gradually expanded across all of Japan (Nihon Shokuniku Kyōgi-kai, 1966, p. 24). In 1975, the Japan Meat Grading Association (JMGA) took over and has subsequently remained in charge of administering meat grading in Japan.

The Japanese standard for ranking beef judges it with a letter score for carcass yield and a number score for quality. For carcass yield, cows are evaluated based on how much meat a carcass yields with ranks of C (under 69 kg), B (69 kg to 72 kg), and A (72 kg and over). The initial meat quality number score ranked meat from one to five, with five being the highest, based on marbling, meat colour and lustre, meat texture and firmness, fat colour and lustre, and fat quality (Nihon Shokuniku Kyōgi-kai, 1966, p. 31). The Japanese Meat Grading Association established several standards for measuring these qualities. The most influential of these standards is the beef marbling standard (BMS), which measures the distribution of intramuscular fat. It assigns a rank of 1 to 5 on carcasses. Those with more intramuscular fat marbling receive higher ranks and are more valuable (JMGA, 2024). Aside from marbling, JMGA also established standards for meat colour and fat colour. The beef colour standard (BCS) ranks meat colour from 1, a bright red, to 7, a dark red, with brighter colours and lower ranks evaluated positively. The beef fat standard (BFS) ranks fat colour from 1, an almost pure white, to 7, a brownish beige, with whiter colours and lower ranks evaluated positively. Once Japan introduced these standards, especially the beef marbling standard, beef breeders and producers pursued beef marbling with a single-mindedness that made Japanese wagyu distinctive and linked high levels of marbling with premium quality.

Japanese wagyu’s devotedness to marbling became an asset in the face of cheaper imported beef as Japan expanded beef imports through the 1980s and 1990s. Wagyu’s high levels of marbling emerged as a distinctive feature of the quality of Japanese wagyu. This positive emphasis on marbling content gained favour in post-war Japan as diets shifted towards fattier and calorie-dense food. For example, fatty tuna (ōtoro) is today seen one of the most exquisite and expensive types of nigiri sushi, but fish mongers viewed fatty tuna with derision through the 1950s and only with shifting taste preferences did fatty tuna come to be viewed with acclaim (Bestor, 2004, p. 142). Positive associations with marbling in fatty tuna buoyed the emphasis on marbling in wagyu as marbling became an indicator of higher quality for both (Peneva, 2008, pp. 88–89). Wagyu emerged as an artisan category of food characterised by domestic production of heirloom beef with a high marbling content.

Covid-19’s impacts

Covid-19’s impacts on food systems were unprecedented. It influenced nearly all aspects of food systems including production, distribution, and consumption. From a political economic perspective, scholars caution that Covid-19 accelerated the extension of corporate control over the food systems (Clapp and Moseley, 2020; van der Ploeg, 2020; Gras and Hernández, 2021). Alongside but in contrast to the trend towards corporate control, Covid-19 also sparked widespread interest in local and alternative food (Bitzer et al., 2024; Jones, Krzywoszynska and Maye, 2022; Kamiyama et al., 2023; Lever et al., 2022; Nemes et al., 2021; Zollet et al., 2021). Disruption to food systems from Covid-19 and effective responses vary widely based on context. In a cross-country comparison, Nemes et al. (2021, p. 595) categorise 13 countries into three different groups characterised by factors such as the prevalence of citizen driven initiatives, affluent consumption, institutional support, and information and communication technology. Focusing on northern England, Lever et al. (2022) examine how the faltering of a top-down managerial approach to food systems created space for a more open place-based approaches to emerge. Drawing on local food systems in the UK, Jones, Krzywoszynska and Maye (2022) emphasise the role of social capital as a key factor that enables transformative resilience in the face of crises like Covid-19. Analysing agroecological farmers in Italy and alternative food networks in Rome, Zollet et al. (2021) demonstrate how local grassroots action provided a crucial source of food security when the mainstream food system faltered during the pandemic. These studies highlight the role of local, alternative, and community-based food systems as a source of resiliency and source of positive transformational.

Our research differs from these studies in three major aspects. First, we are profiling an agrifood industry within Japan, the wagyu industry, as opposed to focusing more broadly on agrifood systems. Doing so enables us better to identify how the industry changed in response to the pandemic. Second, unlike local, alternative, and community-based food systems, Japan’s wagyu industry does not align with progressive politics. Since wagyu is more expensive than non-wagyu and imported meat, wagyu best aligns with artisan food, and production ranges from alternative to industrial operations. Third, Japan’s wagyu industry was widely described in the popular media as suffering through sharp declines during the pandemic (e.g. Asahi Shimbun, 2020a; Asahi Shimbun, 2020b; Kajimoto, 2020). As a result of these three aspects, our study documents how Covid-19 reshaped a significant agrifood industry in Japan with broader relevance to unpacking the complex role of distinct industries and actors within Covid-19’s more general impact on food systems.

Japan received widespread praise from public health experts for suppressing Covid-19 transmission (Tashiro and Shaw, 2020). While most aspects of Japanese food systems endured disruption, large changes emerged with growth in home delivery services and contraction in in-person dining and artisan foods (Schrager and Kondo, 2024). Prior to the pandemic, 25% of wagyu was marketed for in-person dining (Hasegawa, 2020, p. 34). When the pandemic hit, in-person dining decreased both because of government policy and because consumers viewed in-person dining as presenting a greater risk of Covid-19 transmission. Precise statistics on changes in customers and revenue are difficult to obtain, but large surveys reflect these general trends. From the perspective of individual consumers, a survey of over 8,000 Japanese individuals found that during the period of lockdowns they reported eating out 69.0% less, going out for entertainment (including bars, clubs, and shows) 87.9% less, and travelling on vacation 93.8% less than prior to the pandemic (NRI, 2020, p. 25). From the perspective of businesses, a survey of over 11,000 small and middle-size companies found that the category of ‘food and accommodation industries’ reported the worst conditions of the industries surveyed with 80% of companies reporting poor conditions (Daido, 2021, p. 2). Within the broader Japanese economy, dining out sharply declined, presenting a major challenge to a wagyu industry largely dependent on in-person dining.

A 2021 survey of recipients of public agricultural loans with 5,700 respondents, 390 of whom were beef producers, underscored the harsh conditions facing beef producers. An average of 61.0% of beef producers reported a decline in revenue of 10% or greater compared to only 34.3% of overall farmers (JFC, 2021). The category of beef producers encompasses not just wagyu but other beef producers as well. During the peak of Covid-19 lockdown, wagyu production, price per unit, and exports declined; the only bright spot was an increase in beef for home consumption (Hasegawa, 2020). In the case of Okinawa Prefecture’s Ishigaki Beef wagyu brand from Ishigaki Island, Ishigaki Beef sought to reduce its reliance on tourists and in-person dining with a stronger emphasis on marketing for home consumption, local consumers, and crowd funding (Kawanishi and Itō, 2023). Similar shifts took place for Gifu Prefecture’s Higa Beef wagyu brand with a shift away from tourists and towards e-commerce, support from local consumers within Gifu Prefecture, and crowd funding (Hasegawa, 2021). While there are a handful of other studies and media coverage that detail changes for specific brands or the wagyu industry, our article reports on a survey of wagyu brands. By emphasising the difference between brand size, we provide unique insights into the way in which responses to Covid-19 are reshaping the wagyu industry and the brands by which it is animated.

Current conditions

A recent report by the Japanese Ministry of Agriculture, Forestry and Fisheries provides statistical insights into the role of wagyu in Japan. In 2022, Japan consumed 850 metric tonnes of beef, of which 351 metric tonnes (40%) was produced domestically (MAFF, 2024, p. 21). Government statistics divide domestic beef production into categories of wagyu at 171 metric tonnes (49%), mixed breeds (Western breeds crossed with wagyu breeds) at 95 metric tonnes (27%), dairy breeds at 81 metric tonnes (23%), and other at 4 metric tonnes (1%) (ibid., p.21). Even though wagyu accounts for half of domestic production and one fifth of the beef consumed in Japan, wagyu still is significant, because of its economic impact.

In 2022, Japan’s overall revenue from agriculture and livestock was 9 trillion yen (~$60 billion USD) (MAFF, 2023b). The most Japanese of crops, rice, accounts for 1.4 trillion yen of revenue (~$9.3 billion USD, 15.6% of overall revenue). By contrast, livestock accounts for 3.5 trillion yen of revenue (~$25 billion USD, 38.9% of overall revenue). Beef alone accounts for 826 billion yen of revenue (~$5.5 billion USD, 9.2% of overall revenue). By combining overall revenue with government data on production amount and value, we estimate revenue from wagyu to be 500 billion yen (~$3.5 billion USD, 5.6% of overall revenue). The data on production are taken from MAFF (2024, 21) and state that in 2022, Japan produced 171 metric tonnes of wagyu, 95 metric tonnes of mixed, 81 metric tonnes of dairy, and 4 metric tonnes of other. We combined this with data from the same report on the average value of rank A4 wagyu (2,111 yen/kg), rank B3 mixed (1,569 yen/kg), and rank B2 dairy (1,003 yen/kg) (ibid., 22). According to ALIC (2024), the MAFF average rank value slightly underestimates the value of wagyu. Given the available data, we estimate the value of wagyu to be 500 billion yen. This is necessarily a rough estimate but still a useful estimate for gauging the size and importance of wagyu industries in Japan, because it underscores the importance of wagyu for Japan’s agricultural economy.

In terms of producers, there are far more producers of beef for meat consumption than all other livestock producers combined. In 2023, there were 40,000 beef producers with an average of 65 cattle per farm, 14,000 dairy producers with an average of 103 cattle per farm, 3,600 pork producers with an average of 2,500 pigs per farm, 1,800 chicken layer producers with an average of 76,000 chickens per farm, and 2,100 chicken broiler producers with an average of 66,000 chickens per farm (MAFF, 2023a). Compared to the 40,000 beef producers, a little more than half of that number, 21,500 producers, raise dairy, pork, chicken layers, and chicken broilers combined.

Within Japan’s 40,000 beef producers, agricultural statistics do not differentiate between wagyu, mixed, and dairy meat operations. Wagyu producers on average operate on a smaller scale than mixed and dairy meat producers, because wagyu is more lucrative but requires greater labour per animal. However, information is so scant that we cannot even hazard an estimate regarding the statistics of how wagyu producers compare to other beef producers. Such an estimate would be further complicated by operations that raise cattle in more than one category.

Survey methodology

In order to create a survey of Japan’s wagyu industry, we utilised the 2021 Brand Beef Hand Book (sic) compendium of beef brands in Japan (Shokuniku Tsūshin-sha, 2021). The 2021 handbook included descriptions of 377 unique beef brands. For the purposes of our survey, we excluded brands that use non-wagyu breeds or lack production statistics. Of the 224 remaining wagyu brands, 207 (92.4%) use Japanese Black, 4 (1.8%) use a combination of Japanese Black and Japanese Brown, 4 (1.8%) use exclusively Japanese Brown, 8 use Japanese Shorthorn (3.6%), and 1 (0.4%) uses Japanese Polled. In addition, 201 (91.1%) of wagyu organisations protected their brand by utilising schemes such as geographic indications or trademark registrations. The bulk of wagyu brands then use Japanese Black and utilise schemes to protect their brands from infringement.

We distributed the surveys on October 31, 2022 with an initial survey response deadline of November 18. Later, we sent a follow-up postcard thanking participants and extending the deadline to December 5 for those who had yet to complete the survey. The price for wagyu bottomed out in April 2020 before nearly recovering to pre-pandemic levels that year (MAFF, 2024, p. 22). The price for wagyu was higher in 2021 than 2020 but has declined in each subsequent year from 2022 to 2024 (referencing data through September 2024) (ALIC, 2024). The timing of the survey, November 2022, reflects a period when the industry underwent a stiff decline during the pandemic before recovering to near pre-pandemic levels.

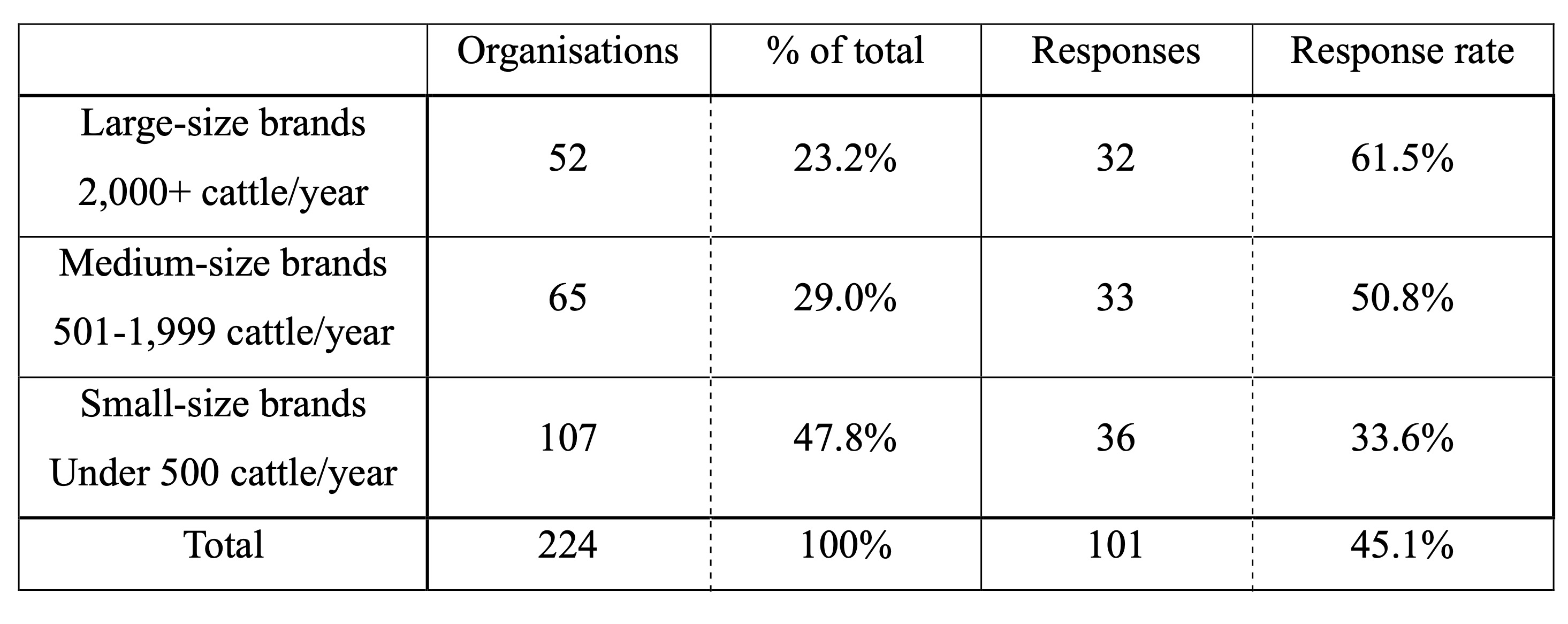

Table 1 illustrates the brands surveyed and response rates of large-size brands (over 2,000 cattle per year), medium-size brands (500 to 2,000 cattle per year), small-size brands (under 500 cattle per year), and overall. To reduce redundancy, these are abbreviated by removing ‘-size’ as small, medium, and large brands respectively. Some of the small brands are unique to a single farm while large brands typically encompass many farms. For example, Kagoshima prefecture’s Kagoshima Kuro-ushi, is the largest brand in the handbook and produces 24,000 cattle per year. As a result, Kagoshima Kuro-ushi produces more than all the small brands combined. For the brands that responded to our survey, the average size of a large brand was 5,500 cattle per year, medium brand was 920 cattle, small brand was 210 cattle. Larger brands were more likely to respond to the survey and smaller brands less likely. Larger brands tend to have greater institutional capacity with dedicated staff for handling administrative requests like surveys, a difference that explains why larger brands were more likely to respond to the survey.

Table 1: Size of wagyu organisations targeted in the survey and response rate

Most publicly available coverage and surveys emphasised the negative impact of the pandemic on wagyu, particularly through the decline of in-person dining (e.g. Lewis, 2020). However, the wagyu industry is difficult to survey, because it consists of numerous actors. While producers raise wagyu cattle, they seldom directly market their cattle. Instead, they typically join a larger organisation that operates under a brand name and orchestrates processing and distribution. Sometimes, producers will produce multiple brands of wagyu on the same farm depending on breed and cattle characteristics. Most brands are organised by a Japanese cooperative (meaning directly affiliated with JA), other types of producer cooperatives, or corporate entities. The handbook identifies a managing entity (kanri-shutai) for each brand. These are the organisations that we surveyed by sending physical surveys through the mail containing a survey, explanation of the project, and prepaid return envelope. While officials at some of these organisations are familiar with changes in the production and distribution of their wagyu brand, some of these organisations have a narrower purview, focusing exclusively on areas such as marketing and public relations. With these variations in mind, we designed our survey to elicit information from those with knowledge of changes in wagyu brands—our emphasis for this project—but also provided viable answers for officials with less comprehensive insights.

The survey consists of two parts that we designed with the aim of identifying Covid-19’s varied impact on wagyu brands. The first and main part asked managing entities to compare their present and pre-pandemic circumstances for 11 different criteria. The criteria are as follows: (1) overall sales revenue, (2) total production volume, (3) total sales volume, (4) sales to restaurants, (5) sales to direct marketing, (6) sales to processors, (7) sales to supermarkets, (8) Internet sales, (9) in-prefecture sales (10) number of certified producers, and (11) number of certified retailers. For each criteria we gave nine possible responses: (1) huge decrease (less than 50% of a typical year), (2) large decrease (50-70% of a typical year), (3) decrease (70-90% of a typical year), (4) little impact (90-110% of a typical year), (5) increase (110-130% of a typical year), (6) large increase (130-150% of a typical year), (7) huge increase (150% or more than a typical year), (8) uninvolved from the outset, and (9) do not know. The second part of the survey invited brands to identify issues that intensified along with the pandemic and areas they would like to see strengthened going forward.

Survey results

Production and sales

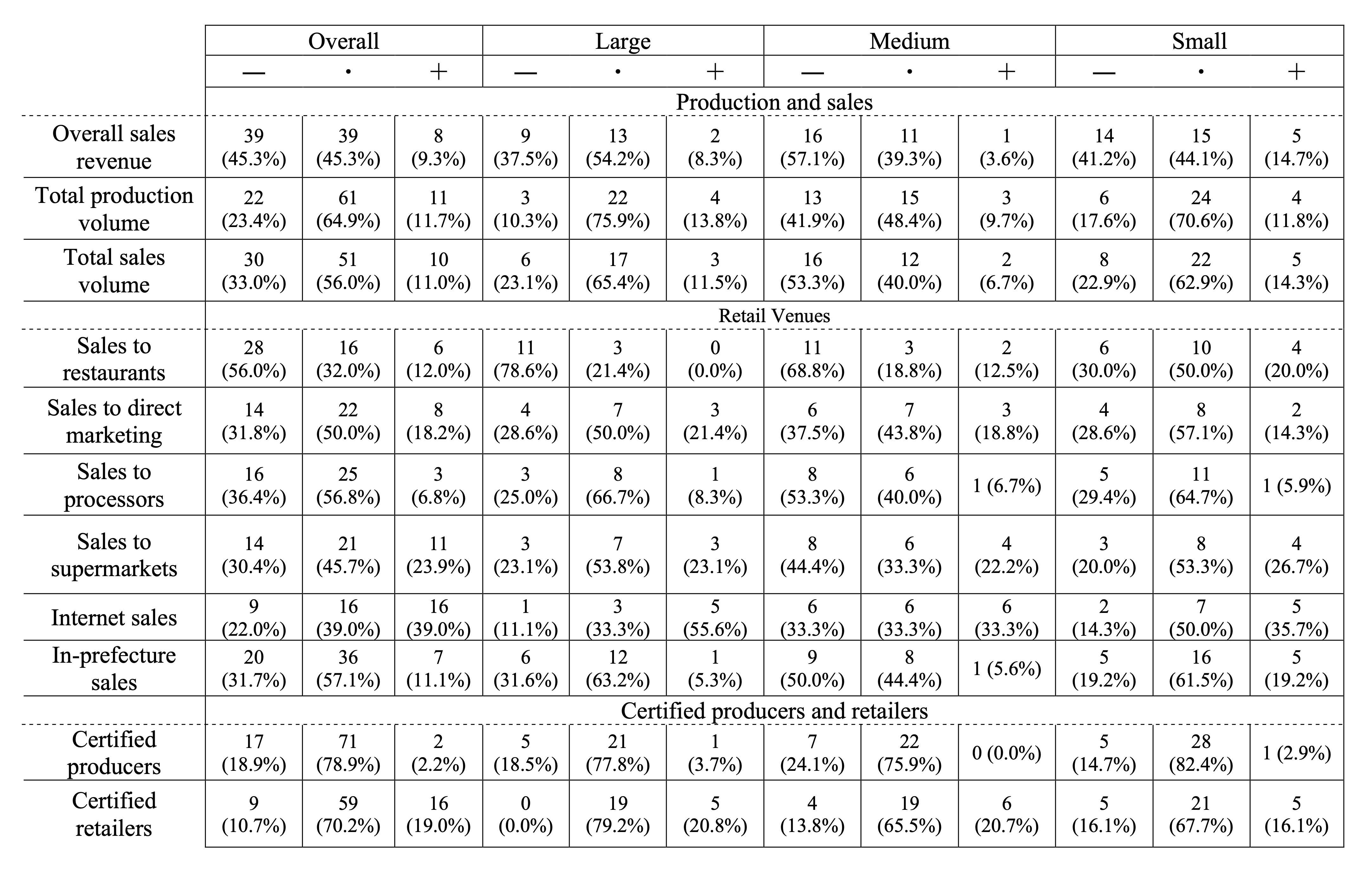

The first part of the survey asked brands to compare their conditions in November 2022 to pre-pandemic conditions (see Table 2). As such, the survey does not ask about the extent to which sales declined during the peak of pandemic shutdowns. Instead, we are asking brands to compare then-current levels of November 2022 to pre-pandemic levels, so the responses should be evaluated as indicating shifts within the industry from prior to the pandemic to when pandemic disruptions were mostly lifted.

In terms of overall production and sales, we asked for brands to report three figures. Comparing these figures, we found that more brands endured a decrease in overall sales revenue (45.3%) than endured a decrease in either total sales volume (33.0%) or production volume (23.4%). The divergence between these figures likely emerges because a decline in value per unit would cause overall revenue to decline even if brands maintained the same level of production and sales.

When differentiating between brand size, more intricate dynamics emerge as medium brands struggled to return to pre-pandemic levels especially when compared to large and small organisations. While overall sales revenue declined for 57.1% of medium brands, it did so for only 41.2% of small brands and 37.5% of large brand. Even more strikingly, medium brands endured widespread declines in total production volume (41.9%) and total sales volume (53.3%). By comparison, small brands were less likely to endure declines in total production volume (17.6%) and total sales volume (22.9%). Likewise, the proportion of large brands was relatively low for declines in total production volume (10.3%) and total sales volume (23.1%). These results that compare the difference between sales revenue, production volume, and sales volume indicate that medium brands faced stiffer headwinds than either small or large brands. In addition, while large brands were better able to maintain production volume, this did not necessarily translate into the same level of sales or revenue as pre-Covid levels.

Table 2: Survey results of wagyu brand sales comparing a typical pre-Covid year to 2022

Retail venues

Since the specific crisis of Covid-19 disrupted food retail venues (Schrager and Kondo 2024), much of the survey focused on whether sales to different retail venues declined, stayed the same, or increased (see Table 2). Among these retail venues, decreases in sales to restaurants was the most widespread with declines in 56.0% of brands. These declines were more widespread for large (78.6%) and medium (68.8%) brands than for small (30.0%) brands. The one retail venue where increases outnumbered decreases was for Internet sales. Overall, 22.5% of organisations reported a decline in sales, 40% no significant changes, and 37.5% reported an increase in Internet-based sales. Increases were especially widespread for large brands (55.6%) compared to medium scale (33.3%) and small (35.7%) brands. These results indicate the shift away from in-person dining and towards online sales that took hold during the peak of the pandemic persisted through November 2022 and could be indicative of broader shifts in retail patterns.

Other shifts in retail venues reveal the complexity of Covid-19’s impact. Regarding supermarkets sales, more brands reported declines (30.4%) than increases (23.9%). However, when we analyse supermarket sales in terms of brand size, it emerges that small and large brands were better able to maintain supermarket sales than medium or small brands. Slightly more small brands reported increases (26.7%) than reported decreases (20.0%). An equal number of large brands reported increases (23.1%) as reported decreases (23.1%). For medium brands, twice as many reported decreases (44.4%) as reported increases (22.2%). The widespread decrease in supermarket sales for medium brands compared to small and large brands is an intriguing result from our survey, but further qualitative research is necessary to determine what distinctive factors of medium brands, if any, caused these results.

Overall, in-prefecture sales declined for 31.7% of brands, which was a more limited decline than the 45.3% of organisations with declines in overall sales value. This indicates that brands were better able to prevent their local sales from declining. Small brands reported the greatest success with maintaining in-prefecture sales as 22.2% or brands reported decreases and 18.5% reported increases. For large brands, 27.8% reported decreases and only 5.6% reported increases. Medium brands reported the most widespread declines as 50.0% reported decreases and only 5.6% reported increases. These responses indicate that small brands were better able to turn to local food systems for support in response to the pandemic.

Certified producers and retailers

Most brands utilise a certification system for producers and retailers affiliated with their brands. Overall, the number of certified producers decreased among 18.9% of brands with decreases of 18.5% for large brands, 24.1% for medium brands, and 14.7% for small brands. Although wagyu producers are declining in number over time, the number of organisations reporting decreases in certified producers indicates that the pandemic led to a sharper than normal decline for some brands. Unlike certified producers, the number of certified retailers increased overall with increases for 19.0% of brands and decreases for 10.7% of brands. Given the disruption from Covid-19, wagyu brands may have emphasised increasing certified retailers as a strategy to provide greater stability. Further qualitative research is needed to explain the increase in certified retailers, but it illustrates how individual brand responses to disruption involve strategic shifts that may run contrary to general expectations.

Issues accompanying the Covid-19 pandemic

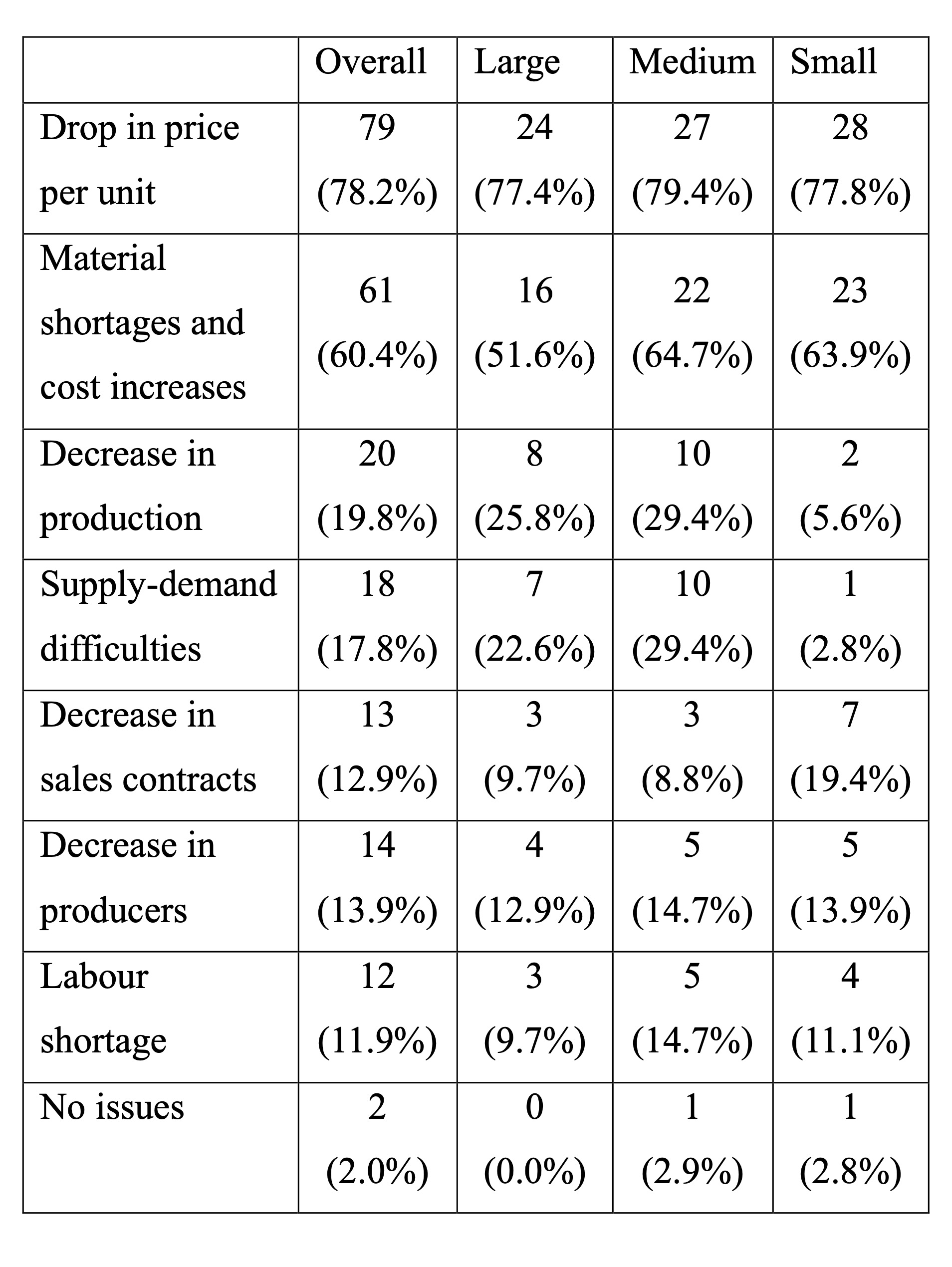

The second part of the survey asked for brands to mark the issues that arose along with the expansion of Covid-19 (see Table 3). On average, brands marked 2.13 issues. Large brands marked the same as the overall average (2.13) while medium brands marked more (2.39) and small brands marked fewer (1.89). Overall, the top issue was the drop in price, which was marked by 77.2% of brands with only slight variation based on brand size. The second issue was material shortages and price increases, which was marked by 61.4% of brands. Large brands (56.3%) marked it slightly less than medium (63.6%) and small (63.9%) brands. While drop in price and material shortages and cost increases were issues widely identified by wagyu brands across all sizes, divergences emerge in subsequent issues.

About a quarter of all large and medium brands identified decreases in production (27.7%) and supply-demand difficulties (24.6%). For small brands, these issues were far less pronounced as only 5.6% identified decreases in production and 2.8% identified supply-demand difficulties. By contrast, small brands were twice as likely to identify a decrease in sales contracts (19.%) as an issue compared to only 9.2% of medium and large brands. These survey responses indicate that medium and large brands had more difficulties maintaining production and balancing supply and demand due to disruption during the pandemic. In contrast, small brands struggled more with disruption to sales contracts.

Table 3: Survey results of issues accompanying the pandemic.

Areas for strengthening going forward

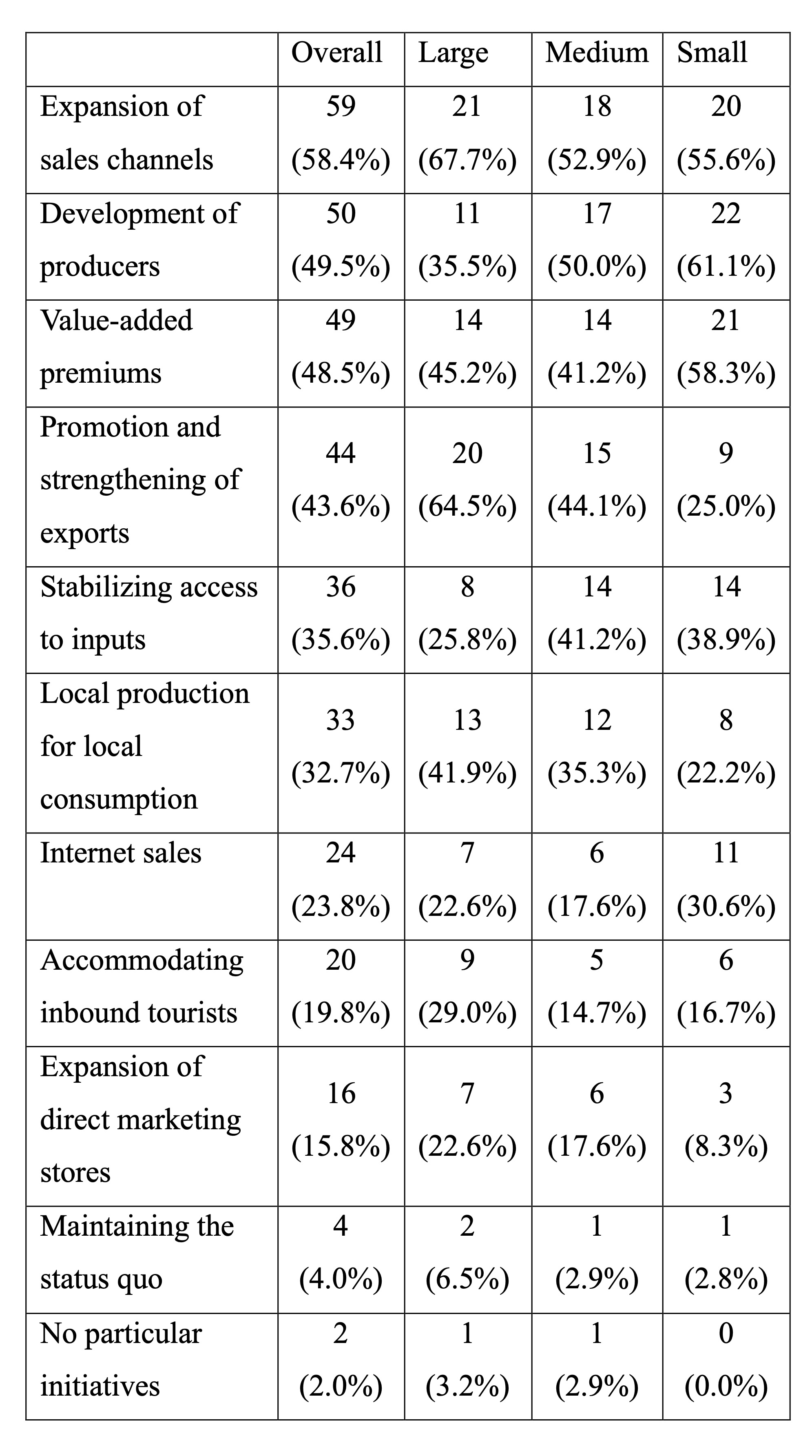

The third part of the survey asked for brands to mark the areas that they would like to see strengthened going forward (see Table 4). On average, brands marked 3.3 areas they would like to see strengthened while large brands (3.6) marked more than medium (3.2) and small (3.1) brands. Compared to the previous questions about issues accompanying the pandemic where only two issues resonated with a wide swath of brands, brands expressed shared affinity for numerous areas to strengthen going forward. While only 2 out of 7 issues broke the 30% threshold for issues arising from the pandemic, 6 out of 10 broke the 30% threshold for areas to strengthen going forward. Since we conducted our survey in November 2022, brands were more focused on forward-looking initiatives than backwards-looking reflection on pandemic-related hardships.

The top area for strengthening across all brands was the expansion of sales channels (58.4%). Large brands sought to strengthen exports (62.5%) more than medium- (45.5%) and significantly more than small (22.2%) brands. Since large brands have the most capacity to pursue exports, we would expect them to express greater interest in strengthening this area. Nearly twice as many large- (39.4%) and middle-size (36.4%) brands sought to strengthen local production for local consumption compared to small-size brands (19.4%). Similarly, the expansion for direct marketing stores was significantly more widespread for large (21.9%) and medium (18.2%) brands than for small (8.3%) brands. We should be cautious about assuming that medium- and large-size brands are more advanced than small-size brands in these areas, especially direct marketing, because it is possible that small-size brands have already taken advantage of these marketing strategies and that is why they do not seek to strengthen them going forward. By contrast, small-size brands sought to strengthen development of producers, value-added premiums, and Internet sales more widely than medium and large brands.

Table 4: Survey results of areas to strengthen going forward.

Discussion of survey results

This survey provides unique insights into both the wagyu industry and how it responded to Covid-19. There is little data available on wagyu as an industry, wagyu when controlling for brand size, or the role of retail venues for wagyu brands. While our survey provides insights into these areas, we should also caution that our survey approach generates unique statistics. First, we tend to report our findings in terms of the proportion of brands that experienced decreases, increases, or little change. For example, 23.4% of brands reported a decrease in production volume (see Table 2). This does not mean that production volume decreased by 23.4%. Rather, 23.4% of brands reported that their sales volume in 2022 declined by over 10% compared to a typical year. In contrast, 64.9% reported less than 10% variation from a typical pre-Covid-19 year and 11.7% reported an increase of over 10%. More than twice as many brands reported a decline than reported an increase.

In reporting the results of our survey, we tend to highlight the difference between brand size. Clear differences emerge between large, medium, and small brands with medium brands facing sharper contraction than large and small brands. Without additional qualitative research, we cannot conclude the reason for widespread decreases among medium brands. Research on the farming of the middle suggests that while middle-size farms are crucial for food systems, they are decreasing at an alarming rate, because middle-size farms lack the flexibility of small farms and the institutional strength of large farm (Lyson, Stevenson and Welsh, 2008). We encourage future research on how Covid-19 impacted both middle-sized wagyu brands and the agriculture of the middle more generally.

Even when controlling for size, important variation emerges at the brand level, and it appears that individual brands are crucial actors in shaping their future trajectories. The role of individual brands is an area that should be better unpacked to understand the extent to which effective brand management practices shape brand trajectories. The pandemic introduced disruption that structurally favoured some brands over others. Such structural advantages include strong online retailing presences, favourable retail contracts, and brand name recognition. In addition to these structural factors, brands had to adjust on the fly to disruption from Covid-19. Brands that successfully navigated the pandemic without significant declines in their business model likely utilised a combination of structural advantages and capacity to respond to disruption. This is another important area of research to continue to unpack so we can better understand Covid-19’s impacts both on wagyu specifically and food systems more broadly.

Since in-person dining is a major source of income for the wagyu industry, its decline had far-reaching impacts from which the industry had still yet to recover as of November 2022. Our analysis shifted beyond overall sales to reveal shifts in other retail venues and how this varied by brand size. Our survey also reveals that brand size influenced the types of issues that brands identified as arising from the pandemic and the areas that brands sought to strengthen going forward. The variation by and within brand size reinforces the myriad of ways that Covid-19 impacted different organisations even when operating in the same industry. These dynamics reinforce the importance of carefully examining the processes that reshape food systems and the factors that foster food system resilience.

Conclusion: Contextualising disruption and recovery from Covid-19

The pandemic disrupted food systems across the world and reshaped food systems in unprecedented directions. Agrifood scholars are continuing to unpack the implications of the pandemic. Agrifood scholars have noted how the pandemic exacerbated the general crisis of the corporate food regime with rising food insecurity and tightening corporate control (Clapp and Moseley, 2020; van der Ploeg, 2020). They have also examined how the pandemic underscored the crucial role of local, community-based, and alternative food in bolstering food system resilience (Jones, Krzywoszynska and Maye, 2022; Lever et al., 2022; Nemes et al., 2021; Zollet et al., 2021). Shifting away from clear examples of the deepening or reversal of the corporate food regime, our research on Japan’s wagyu industry delves into the messy middle, where Covid-19’s impacts are evident but also difficult to overgeneralise given the complex disruption experienced and responses taken by diverse actors within a broader industry. As agrifood scholars continue to sift through the longer-term implications of Covid-19, its varied impacts within industries has broader implications for understanding the new baselines that emerge after the pandemic and its complex intersections with the deeper crisis of the corporate food regime.

Acknowledgements:

We would like to acknowledge and thank the officials from brands that took the time to respond to our survey. This work was supported by JSPS KAKENHI (Grant-in-Aid for Early-Career Scientists) Grant Number 22K14955.

References

ALIC (2024) Beef Price Trend. Available at: https://lin.alic.go.jp/alic/statis/dome/data2/i_pdf/2060a-2110a.pdf.

Altieri, M.A. and Nicholls, C.I. (2020) “Agroecology and the reconstruction of a post-COVID-19 agriculture,” The Journal of Peasant Studies, 47(5), pp. 881–898. Available at: https://doi.org/10.1080/03066150.2020.1782891.

Asahi Shimbun (2012) “I am indeed the father: The ancestor of 99.9% of Japanese Black cows (Japanese: Ware koso kuroge wagyū no chichi — hahaushi kyūjūkyū-ten kyū pāsento ga shison),” 2 March, p. 38.

Asahi Shimbun (2020a) “Covid’s direct hit on Agriculture; Wagyu Beef Prices Plummet; ‘Monthly Revenue Loss of 1 Million Yen’ (Japanese: korona, nōgyō chokugeki; wagyū kakaku kyūraku ’genshū tsuki 100 man-en’),” 20 April, p. 25.

Asahi Shimbun (2020b) “Wagyu Beef Prices Plummet; ‘We’re Barely Making a Living’ (Japanese:wagyū no kakaku, kyūraku ’tabete iku no ga yatto’),” Morning western edition, 4 May, p. 19.

Bestor, T.C. (2004) Tsukiji: The fish market at the center of the world. Berkeley; London: Univ of California Press.

Bitzer, V. et al. (2024) “Vulnerability and resilience among farmers and market actors in local agri-food value chains in the face of COVID-19 disruptions: findings from Uganda and Kenya,” Food Security, 16(1), pp. 185–200. Available at: https://doi.org/10.1007/s12571-023-01414-z.

Clapp, J. and Moseley, W.G. (2020) “This food crisis is different: COVID-19 and the fragility of the neoliberal food security order,” The Journal of Peasant Studies, 47(7), pp. 1393–1417. Available at: https://doi.org/10.1080/03066150.2020.1823838.

Daido (2021) Small and medium-sized business owner questionnaire “Daido Life Survey” (Japanese: Chūshōkigyō keiei-sha ankēto ʻdaidō seimei sābeiʻ). Daido Life Insurance Company. Available at: https://www.daido-life.co.jp/company/news/2021/pdf/210119_news.pdf.

Edelman, M. and Wolford, W. (2017) “Introduction: Critical Agrarian Studies in Theory and Practice: Symposium: Agrarianism in Theory and Practice Organisers: Jennifer Baka, Aaron Jakes, Greta Marchesi and Sara Safransky,” Antipode, 49(4), pp. 959–976. Available at: https://doi.org/10.1111/anti.12326.

Farrer, J. (2022) “Sustainable neighbourhood gastronomy: Tokyo independent restaurants facing crises,” Asia Pacific Viewpoint, 63(3), pp. 396–410. Available at: https://doi.org/10.1111/apv.12339.

Gotoh, T. et al. (2018) “The Japanese Wagyu beef industry: current situation and future prospects — A review,” Asian-Australasian Journal of Animal Sciences, 31(7), pp. 933–950. Available at: https://doi.org/10.5713/ajas.18.0333.

Gras, C. and Hernández, V. (2021) “Global agri‐food chains in times of COVID‐19: The state, agribusiness, and agroecology in Argentina,” Journal of Agrarian Change, 21(3), pp. 629–637. Available at: https://doi.org/10.1111/joac.12418.

Hasegawa K. (2020) “Trends: Fluctuations in Wagyu Supply and Demand Amid the COVID-19 Pandemic (Jōsei: Korona-ka ni okeru wagyū jukyū no hendō),” Nōrin kin’yū, 73(9), pp. 508–513.

Hasegawa K. (2021) “Wagyu Supply and Demand and Regional Responses During the COVID-19 Pandemic (Korona-ka ni okeru wagyū jukyū to sanchi taiō),” Nōrin kin’yū, 74(8), pp. 380–392.

Hudson, M. and Muñoz Fernández, I.M. (2023) “Henceforth fishermen and hunters are to be restrained: towards a political ecology of animal usage in premodern Japan,” Asian Archaeology, 24(2), pp. 183–201. Available at: https://doi.org/10.1007/s41826-023-00072-6.

Ishihara, Y. (2023) Branded beef as a cultural asset (Japanese: Kyōyō to shite no burando ushi). Tokyo: Gentosha. Available at: https://ci.nii.ac.jp/ncid/BD04106213 (Accessed: June 24, 2024).

JFC (2021) Agricultural Business Conditions Survey January 2021 (Nōgyō keikyō chōsa Reiwa 3-nen 1-gatsu). Japan Finance Corporation. Available at: https://www.jfc.go.jp/n/findings/pdf/topics210315a.pdf.

JMGA (2024) Beef carcass trading standards (Japanese:Ushi edaniku torihiki kikaku) (Japan Meat Grading Association). Available at: https://www.jmga.or.jp/standard/beef/ (Accessed: September 18, 2024).

Jones, S., Krzywoszynska, A. and Maye, D. (2022) “Resilience and transformation: Lessons from the UK local food sector in the COVID‐19 pandemic,” The Geographical Journal, 188(2), pp. 209–222. Available at: https://doi.org/10.1111/geoj.12428.

Kajimoto, T. (2020) “From wagyu beef to melons, Japan’s $2.2 trillion virus rescue piques struggling firms,” Reuters, 4 June. Available at: https://www.reuters.com/article/us-health-coronavirus-japan-stimulus-idUSKBN23B00P (Accessed: March 26, 2023).

Kamiyama, C. et al. (2023) “Longitudinal analysis of home food production and food sharing behaviour in Japan: multiple benefits of local food systems and the recent impact of the COVID-19 pandemic,” Sustainability Science, 18(5), pp. 2277–2291. Available at: https://doi.org/10.1007/s11625-023-01363-8.

Kawanishi M. and Itō M. (2023) “Efforts to Address the Decline in Beef Consumption During the COVID-19 Pandemic: How Ishigaki Beef Overcame the Crisis (Korona-ka ni okeru gyūniku no shōhi-gen ni taisuru torikumi ni tsuite: Ishigaki gyū ga korona-ka o norikoeru tame ni),” Chikusan no Jōhō, (403), pp. 57–64.

Lever, J. et al. (2022) “Working across boundaries in regional place-based food systems: Triggering transformation in a time of crisis,” Cities, 130, p. 103842. Available at: https://doi.org/10.1016/j.cities.2022.103842.

Lewis, L. (2020) “Coronavirus serves up a surplus of Wagyu beef,” Financial Times, 3 April. Available at: https://www.ft.com/content/bb540839-2f63-43bc-897c-b73b2d9f6dc7 (Accessed: February 6, 2025).

Lichten, J. and Kondo, C. (2020) “Resilient Japanese Local Food Systems Thrive during COVID-19: Ten Groups, Ten Outcomes (十人十色 jyu-nin-to-iro),” Japan Focus, 18(18), p. 8.

Lyson, T.A., Stevenson, G.W. and Welsh, R. (2008) Food and the mid-level farm : renewing an agriculture of the middle. Cambridge, Mass: MIT Press.

MAFF (2023a) Livestock statistics (As of 1 Feb 2023) (Japanese: Chikusan tōkei (Reiwa 5-nen 2-gatsu 1-nichi)). Available at: https://www.maff.go.jp/j/tokei/kekka_gaiyou/tiku_toukei/r5/ (Accessed: December 7, 2024).

MAFF (2023b) Total Agricultural Output and Agricultural Production Income (National) in 2022 (Japanese: Reiwa yon-nen nōgyō sōsanshutsugaku oyobi seisan nōgyō shotoku (zenkoku)). Available at: https://www.maff.go.jp/j/tokei/kekka_gaiyou/seisan_shotoku/r4_zenkoku/index.html (Accessed: December 7, 2024).

MAFF (2024) The situation for livestock and dairy (Japanese: Chikusan・rakunō o meguru jōse).

Matsumoto, S. and Otsuki, T. (2024) “How did Japanese households change their food purchasing behaviour at the initial period of the COVID-19 outbreak?,” Cogent Economics & Finance, 12(1), p. 2404709. Available at: https://doi.org/10.1080/23322039.2024.2404709.

Motoyama, M., Sasaki, K. and Watanabe, A. (2016) “Wagyu and the factors contributing to its beef quality: A Japanese industry overview,” Meat Science, 120, pp. 10–18. Available at: https://doi.org/10.1016/j.meatsci.2016.04.026.

Nemes, G. et al. (2021) “The impact of COVID-19 on alternative and local food systems and the potential for the sustainability transition: Insights from 13 countries,” Sustainable Production and Consumption, 28, pp. 591–599. Available at: https://doi.org/10.1016/j.spc.2021.06.022.

Nihon Shokuniku Kyōgi-kai, (1966) The Realities of the Meat Retail Industry (Japanese: Shokuniku hanbaigyō no jissai). Shokuniku Tsūshinsha. Available at: https://dl.ndl.go.jp/pid/3442683/1/19 (Accessed: June 27, 2024).

NRI (2020) The Impact of COVID-19 on Consumption Related to Dining Out, Entertainment, and Travel, and Recovery Strategies (Shingata Korona Uirusu ga Gaishoku, Goraku, Ryokō Kanren Shōhi ni Ataeta Eikyō to Kaifuku-saku). Nomura Research Institute. Available at: https://www.nri.com/content/900032302.pdf.

Peneva, T.V. (2008) The invention of wagyu beef and contemporary meat-eating practices in Japan : an anthropological study of Omi beef production and consumption. Ph.D. Thesis. Kyoto University.

van der Ploeg, J.D. (2020) “From biomedical to politico-economic crisis: the food system in times of Covid-19,” The Journal of Peasant Studies, 47(5), pp. 944–972. Available at: https://doi.org/10.1080/03066150.2020.1794843.

Schrager, B. and Kondo, C. (2024) “A critical agrarian approach to food crises: Social distance as a specific food crisis arising from the COVID-19 pandemic in Japan,” Environment and Planning E: Nature and Space, 7(2), pp. 681–701. Available at: https://doi.org/10.1177/25148486231194835.

Shokuniku Tsūshin-sha (2021) Brand Beef Hand Book (Japanese: Gyūniku Handobukku). Osaka: Shokuniku Tsūshin-sha.

Tashiro, A. and Shaw, R. (2020) “COVID-19 Pandemic Response in Japan: What Is behind the Initial Flattening of the Curve?,” Sustainability, 12(13), p. 5250. Available at: https://doi.org/10.3390/su12135250.

Zollet, S. et al. (2021) “Towards Territorially Embedded, Equitable and Resilient Food Systems? Insights from Grassroots Responses to COVID-19 in Italy and the City Region of Rome,” Sustainability, 13(5), p. 2425. Available at: https://doi.org/10.3390/su13052425.

Article copyright Benjamin Schrager and Hideaki Jindai.

The electronic journal of contemporary japanese studies was founded on 9 January 2001.

Page created 16 December 2019, last modified 16 December 2019.

Email the webmaster if you have any problems.

Copyright electronic journal of contemporary japanese studies.